All Categories

Featured

Table of Contents

- – How much does Term Life Insurance With Fixed P...

- – How do I compare No Medical Exam Level Term Li...

- – How much does Term Life Insurance With Fixed ...

- – Can I get Level Term Life Insurance Quotes on...

- – Who provides the best Level Term Life Insura...

- – Why should I have Level Premium Term Life In...

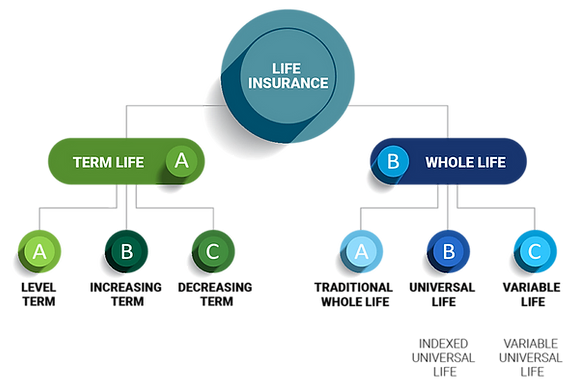

Level term life insurance policy is just one of the most inexpensive protection alternatives on the marketplace because it supplies basic protection in the kind of survivor benefit and just lasts for a collection duration of time. At the end of the term, it runs out. Whole life insurance policy, on the various other hand, is significantly more expensive than degree term life because it does not run out and features a cash money worth function.

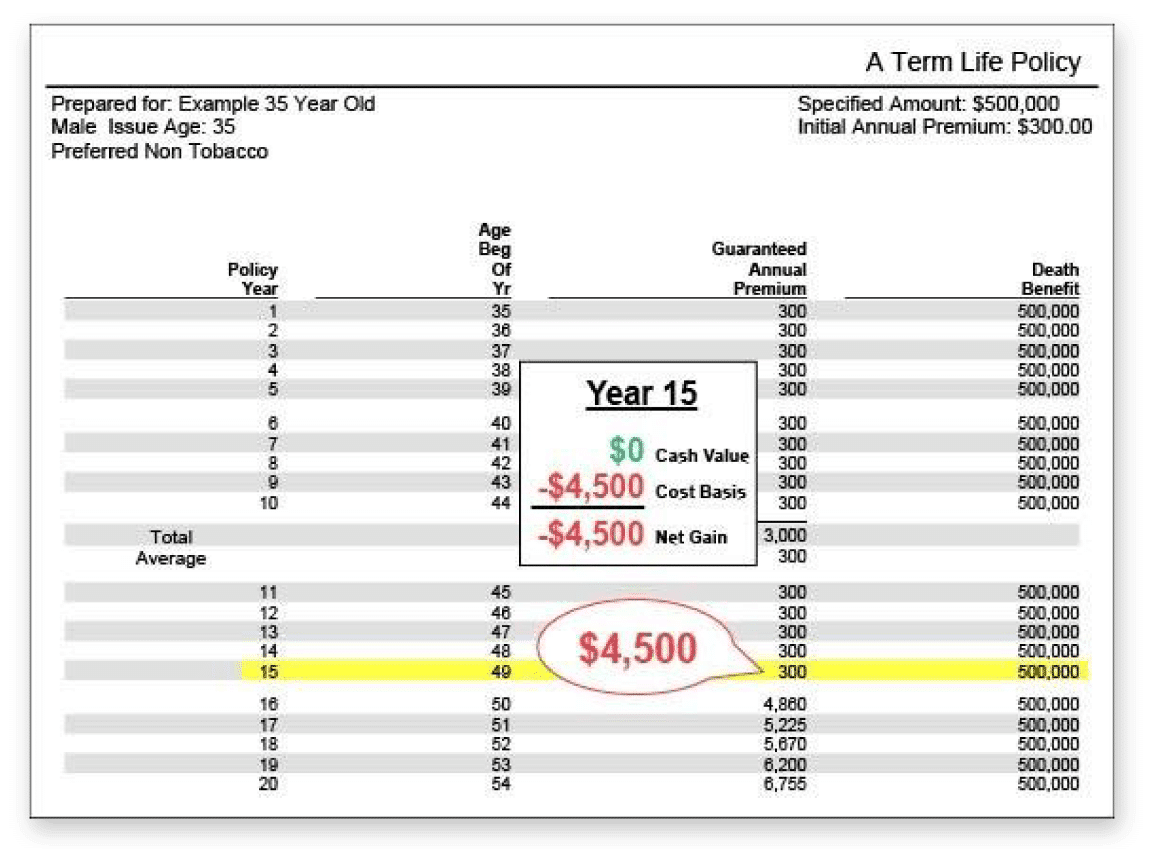

Rates may vary by insurer, term, protection quantity, health course, and state. Not all plans are readily available in all states. Price image valid as of 10/01/2024. Level term is a wonderful life insurance policy alternative for most people, however relying on your coverage requirements and individual scenario, it may not be the very best fit for you.

How much does Term Life Insurance With Fixed Premiums cost?

Yearly renewable term life insurance has a regard to only one year and can be renewed annually. Annual sustainable term life costs are originally reduced than level term life costs, however costs increase each time you renew. This can be an excellent option if you, as an example, have simply stop smoking and need to wait two or 3 years to look for a degree term plan and be qualified for a reduced price.

With a lowering term life policy, your fatality benefit payment will reduce in time, yet your payments will stay the very same. Lowering term life policies like mortgage defense insurance policy typically pay out to your lender, so if you're trying to find a policy that will pay out to your enjoyed ones, this is not a good fit for you.

Boosting term life insurance policies can aid you hedge versus inflation or strategy financially for future children. On the various other hand, you'll pay more in advance for much less insurance coverage with a boosting term life plan than with a degree term life policy. If you're not exactly sure which type of policy is best for you, collaborating with an independent broker can aid.

How do I compare No Medical Exam Level Term Life Insurance plans?

When you've chosen that degree term is ideal for you, the next step is to acquire your policy. Right here's how to do it. Compute how much life insurance you need Your insurance coverage quantity need to attend to your household's long-term economic demands, consisting of the loss of your earnings in the event of your fatality, as well as financial debts and day-to-day costs.

As you seek means to secure your financial future, you've likely encountered a wide array of life insurance coverage alternatives. Picking the appropriate insurance coverage is a big decision. You wish to locate something that will help support your liked ones or the reasons important to you if something occurs to you.

Many individuals lean towards term life insurance for its simplicity and cost-effectiveness. Degree term insurance, however, is a kind of term life insurance policy that has regular settlements and a changeless.

How much does Term Life Insurance With Fixed Premiums cost?

Level term life insurance is a subset of It's called "level" due to the fact that your premiums and the advantage to be paid to your liked ones remain the same throughout the contract. You won't see any type of modifications in expense or be left questioning its value. Some agreements, such as yearly sustainable term, may be structured with premiums that boost gradually as the insured ages.

Repaired fatality benefit. This is likewise established at the start, so you can know exactly what fatality benefit amount your can anticipate when you pass away, as long as you're covered and updated on premiums.

Can I get Level Term Life Insurance Quotes online?

You agree to a fixed costs and death advantage for the duration of the term. If you pass away while covered, your fatality benefit will be paid out to liked ones (as long as your premiums are up to date).

You may have the choice to for one more term or, most likely, renew it year to year. If your agreement has actually an assured renewability condition, you might not require to have a brand-new medical examination to maintain your coverage going. Nonetheless, your costs are likely to boost because they'll be based on your age at revival time. Best value level term life insurance.

With this choice, you can that will last the remainder of your life. In this instance, again, you might not need to have any type of new medical examinations, yet premiums likely will climb due to your age and brand-new insurance coverage. Different firms supply numerous choices for conversion, make sure to understand your options before taking this action.

Consulting with an economic consultant additionally might aid you establish the course that aligns best with your general approach. Most term life insurance policy is level term throughout of the contract duration, however not all. Some term insurance might include a costs that increases over time. With decreasing term life insurance policy, your death advantage drops over time (this kind is commonly gotten to especially cover a lasting debt you're repaying).

Who provides the best Level Term Life Insurance Benefits?

And if you're established for sustainable term life, after that your costs likely will go up yearly. If you're exploring term life insurance and intend to ensure uncomplicated and foreseeable economic protection for your family members, level term may be something to take into consideration. As with any kind of type of coverage, it may have some constraints that don't fulfill your demands.

Generally, term life insurance is more cost effective than permanent protection, so it's a cost-effective means to secure monetary protection. Versatility. At the end of your agreement's term, you have multiple alternatives to continue or carry on from protection, typically without needing a clinical exam. If your budget plan or insurance coverage requires modification, survivor benefit can be reduced in time and lead to a lower costs.

Why should I have Level Premium Term Life Insurance?

As with other kinds of term life insurance coverage, when the contract ends, you'll likely pay greater costs for insurance coverage due to the fact that it will recalculate at your present age and health and wellness. Repaired protection. Degree term uses predictability. However, if your economic circumstance modifications, you might not have the required coverage and could have to purchase added insurance.

That doesn't mean it's a fit for everyone. As you're shopping for life insurance policy, right here are a few key factors to consider: Budget plan. One of the advantages of level term insurance coverage is you understand the price and the fatality advantage upfront, making it easier to without stressing over rises over time.

Age and health. Generally, with life insurance coverage, the healthier and more youthful you are, the a lot more affordable the insurance coverage. If you're young and healthy and balanced, it may be an attractive alternative to secure in low premiums now. Financial obligation. Your dependents and economic obligation contribute in determining your insurance coverage. If you have a young household, for example, level term can help supply financial backing during important years without paying for insurance coverage longer than needed.

{kind=link}

Table of Contents

- – How much does Term Life Insurance With Fixed P...

- – How do I compare No Medical Exam Level Term Li...

- – How much does Term Life Insurance With Fixed ...

- – Can I get Level Term Life Insurance Quotes on...

- – Who provides the best Level Term Life Insura...

- – Why should I have Level Premium Term Life In...

Latest Posts

Burial Insurance Life

Life Insurance For Burial Costs

Funeral Insurance Reviews

More

Latest Posts

Burial Insurance Life

Life Insurance For Burial Costs

Funeral Insurance Reviews